Many taxpayers are seeing their tax refunds reduced or worst still they have a tax bill this year, resulting in a large number of people feeling disappointed. Our team at MJJ have identified several factors that could be contributing to a diminishing return, this year and in future.

Employer withholding rates now adjusted to avoid excess tax being taken out.

When asking any question about a potential tax return it is important to first acknowledge that it is your money that is being refunded. The amount that most taxpayers call a refund is simply the excess money that has been withheld from their weekly, fortnightly, or monthly wages by their employer to help that individual meet their annual tax obligation. This withheld amount is known as your Pay As You Go (PAYG) withholdings.

It is important to understand this because technically the best type of tax refund is no refund at all. If your employer withholds the exact amount of tax each pay to meet your tax obligation, it provides you with the maximum amount of your salaries and wages to spend, save, or invest throughout the year without leaving you with a tax bill.

The ATO is aware of this fact, and in recent years have made a continuous effort to calculate the withholding rates that are mandated each year as accurate as possible. While this achieves the ATO’s underlying aim of provide taxpayers with as much of their income as possible, it does mean that taxpayers are no longer receiving large tax refunds due to excess tax withheld from ordinary employment income.

Claiming the tax-free threshold from 2 or more employers

As discussed above, employers acting on the ATO’s mandated behalf, aim not to withhold more than is required from their employee’s income. Part of achieving this goal is to consider that all Australian citizens are not required to pay tax on their first $18,200 of income. This is why all employers will ask you if you wish to claim ‘the tax-free threshold’ on your tax declaration when you start in a new job. However, each Australian citizen is only entitled to one tax free threshold.

This can create a situation for those generating income for more than one employer where not enough income is being withheld from their pay. This stems from both employers working under the assumption you are claiming the $18,200 tax-free threshold on the income they pay you, reducing the amount of tax they withhold, when in fact it is being claimed by another employer.

While there is nothing technically wrong with this situation, it will mean that one or more employers will not have withheld enough tax from your income, resulting in a lower tax refund or a tax bill at the end of they year. To avoid this situation, you can simply choose one employer you wish to claim the tax-free threshold with and inform your payroll officer at the other organisation/s that you do not wish to claim the tax-free threshold.

HECS debt not notified on TFN declaration.

The tax-free threshold is not the only item that can determine if an employer is withholding enough tax throughout the year. A Highter Education Loan Program or HELP Debt, (previously known as HECS debt) can also dramatically affect the accuracy of the tax being withheld from your income and ultimately the size of your tax refund or bill at the end of the year.

Employers will ask you if you have any HELP Debt alongside the tax-free threshold question on your tax declaration form. Indicating ‘yes’ to this question if it is applicable will allow your employer to withhold an additional amount from your income as it is generated to meet your additional obligation to the ATO. A HELP repayment obligation can be substantial, with repayments rates starting a 1% of total repayment income for those earning between $51,550 – $59,518 and topping out at 10% of total repayment income for individuals earning grater that $151,201 in the 2023-24 financial year.

For example, an individual earning $75,000 who failed to disclose to their employer that they had a HELP loan could expect to pay an additional $2,625 at tax time to meet their repayment obligation. For more information on how much you HELP/HECS costs your per week click here.

If you have a HELP loan and find you are receiving tax bills each year it may be worth investigating if your employer is withholding repayments as part of your PAYG withholdings.

Alternatively, if you suspect that your HELP/HECS loan has been recently paid off, it may pay to check that your employer is aware of this and ceases to withhold the extra tax from your income.

Earning interest income on a bank account

As we are all aware, interest rates have steadily risen since the RBA began targeting the high rate of inflation left in COVID-19 wake. For many of us this has meant a steep rise in our mortgage repayment, but it has also seen the return of healthy interest income on our savings accounts. The increase in interest being paid on savings may in fact be substantial enough to decrease taxpayers tax refunds. This is a result of interest income being predominantly paid in full, leaving the burden of managing potential tax payable on this income up to the taxpayer. While this may seem benign, at tax time the additional untaxed income can quickly contribute to a higher tax payable.

Take for example an individual earning $75,000 who has received an additional $500 in interest during the 2023 tax year. This individual can expect to pay and additional $162.50 in income tax and have their Medicare Levy increased by $10, making a total increase in tax payable of $172.50.

No middle-income tax offset anymore.

The Low-Middle Income Tax Offset (LMITO) was introduced by the Scott Morrison administration in 2018 as a temporary measure to help households and low-income earners with the rising cost of living pressures. This offset in effect provided taxpayers earning between $37,000 and $126,000 with as much as a $1,500 credit towards their annual tax bill. In many cases the amount that was offset by the LMITO had already been withheld from the taxpayers’ wages by their employer, therefore making the LMITO an effective tax refund credit.

Now that the LMITO has been discontinued a greater portion of the amount withheld by employers from your wages is required to meet the tax requirements. For those earning between $37,000 and $126,000 a year, this means lowering any potential tax refund by as much as $1,500.

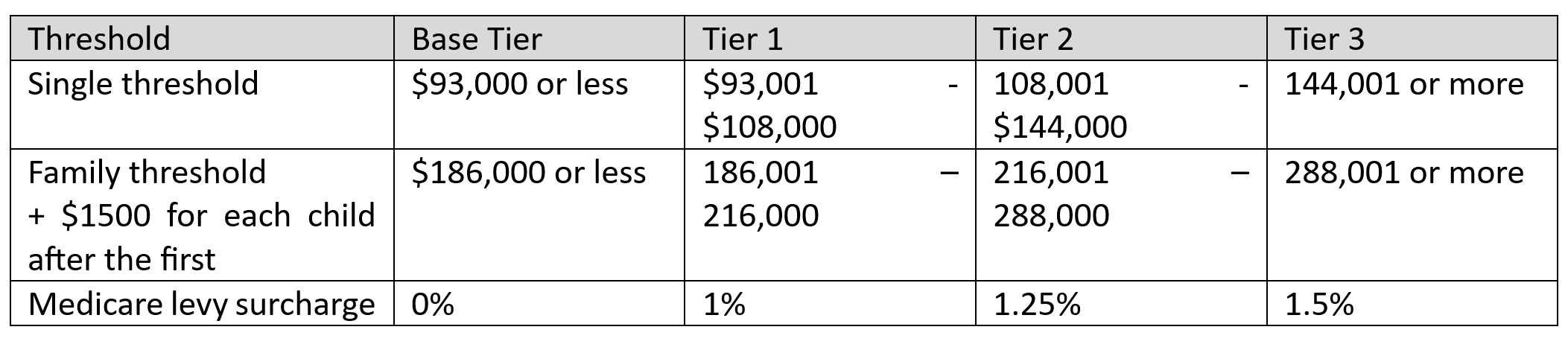

Going over the Medicare levy surcharge threshold.

The Medicare levy is something that most Australian tax residences pay to contribute to the free health care system operating in Australia. However, as your income increases it is important to be aware of the Medicare levy surcharge (MLS). The MLS is a progressive tax that is levied on individuals and families with income greater than $93,000 and $186,000 respectively for the 2023-24 tax year. The progression of the tax, outlined in the table below, is avoidable if you or family has an appropriate level of private patient hospital cover.

For individuals and families earning amounts greater than the MLS threshold and looking to avoid paying the MLS must meet two criteria that quantifies an ‘appropriate level of private patient hospital cover’.

Firstly, the type of cover that is held must be Patient Hospital Cover. This pays for some or all the costs of hospital treatment as a private patient, including doctors’ fees and hospital accommodation. Patient Hospital Cover is the only form of private health insurance that is required to avoid paying the MLS. General cover, commonly known as ‘extras’, is not private patient hospital cover. General Cover Insurance covers items such as optical, dental, physiotherapy or chiropractic treatment and has no effect on determining if a taxpayer is liable for the MLS.

The second element is Patient Hospital Cover excess. For singles, an appropriate level of cover must have an excess of $750 or less. For couples or families an appropriate level of cover must have an excess $1,500 or less.

Reduced deduction for work from home expenses i.e. can claim cents per hour plus some costs – it’s all encompassing now.

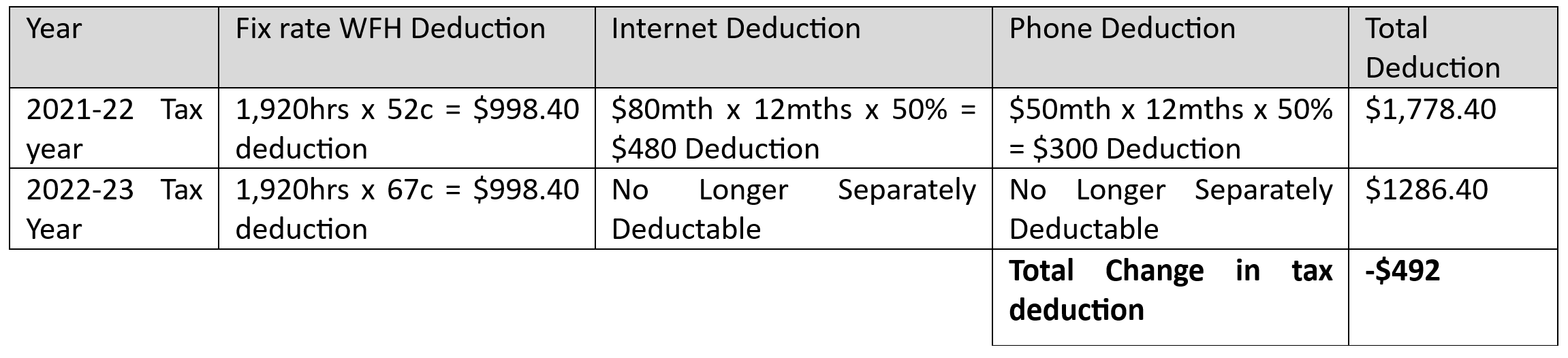

Lastly the ATO’s revision of work from home deductions have reduced the amount that is commonly deductible, lowering tax refunds for many full-time and part-time work from home employees. The revision saw the fixed rate method increased from 52 cents to 67 cents for the 2022-23 tax year. While this might seem positive, the ATO also expanded what the fixed rate method includes, adding Internet, Mobile & Home Phone, Electricity, Gas, Computer Consumables (printer ink and paper), and stationery expenses to the inclusions of the fix rate method.

This means that you can no longer claim any of these expenses in conjunction with the fixed rate method. For many this has reduced work from home deductions dramatically.

Let’s take for example an individual working from home full-time (or 1,920 hours a year) who pay $80 for internet and $50 for phone a month and uses 50% of their phone and internet for work purposes. The table below shows how the revised WFH rates affect the deductible expenses.

This simple example shows how without considering any deductions other than phone and internet, the revised work from home rate has reduced the tax deductible amount by more than 27%. While the nature and numbers of each person claiming a deduction for work from home changes, the outcome from the revised rate are consistent.

When viewed in isolation the 7 different factors explained above may seem trivial, but combined they can impact how your tax is calculated and how much is ultimately paid or refunded come tax time. So, if you were unhappy with your tax refund or bill this year, we encourage you to revisit each section to ensure you understand its effects and our recommendations on how you might get on top of these issues before 30 June.

Comments are closed.