If you’re a business in Queensland and you employ workers, you must insure them against work-related injury or illness with an accident insurance policy. This requires that all PAYG employees and some contractors are provided WorkCover.

WorkCover Queensland (provided by the Qld government) is the exclusive provider of accident insurance for work-related injuries in Queensland, except for self-insured businesses.

To understand who you should be covering for workers’ compensation – and so you can declare your wages accurately – you need to know exactly is considered your employee.

Contractors verse Employees

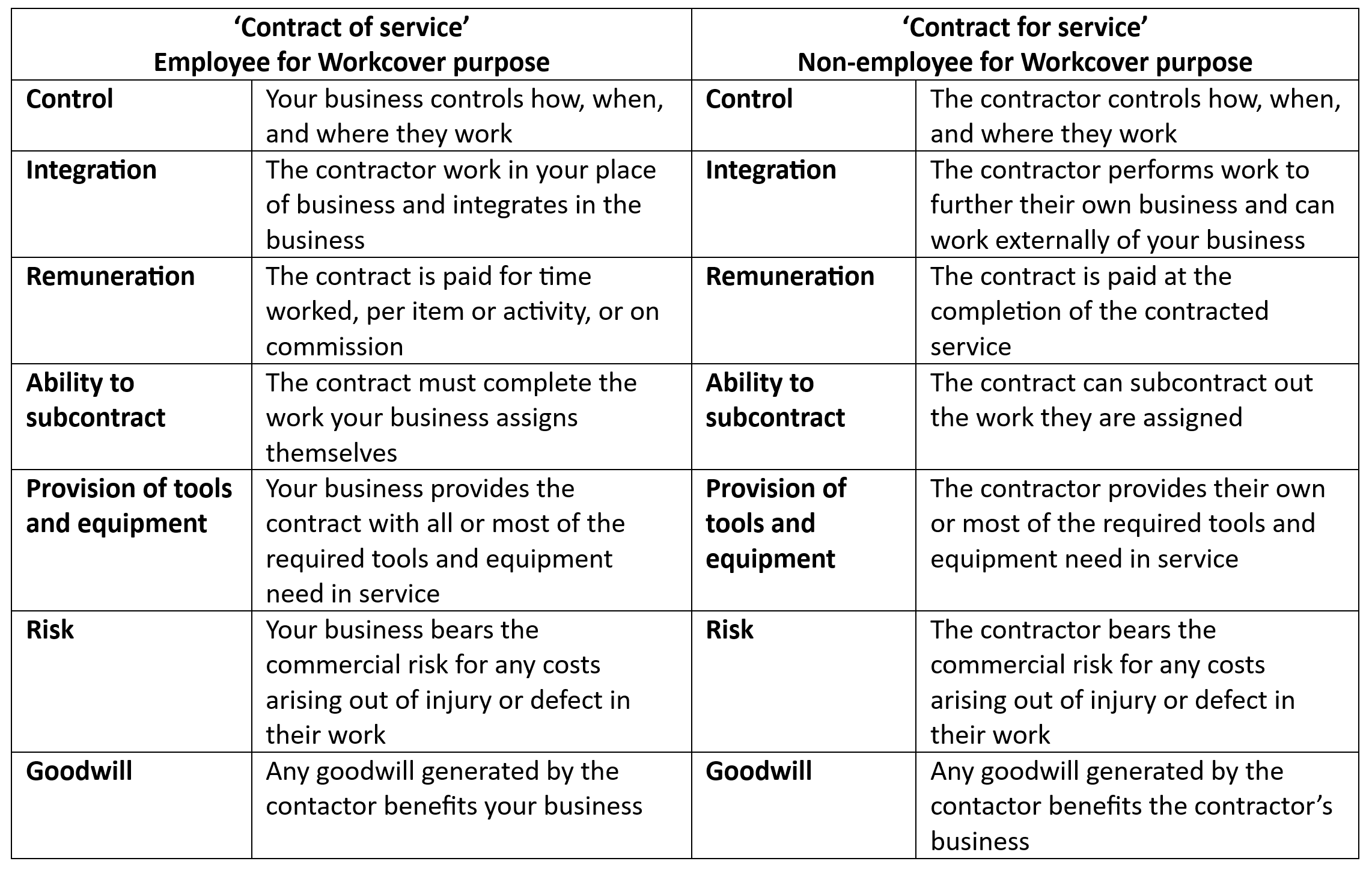

A common and unknowing error made by businesses is failing to provide work cover for their ‘contracts’ who are classified under the Workers’ Compensation and Rehabilitation Act 2003 as employees. The important distinction that determines if a contract is and ‘employee’ is whether they have been contracted for as a ‘contact of service’ or a ‘contract for service’.

So how can you make the distinction for the contactors in your business? The ATO has advised using six (6) key indicators which form a framework for classifying contracts which we have summarized below but can be found in full here.

It should be noted here that only an individual contracting as a sole trader is subject to this test. If a contract is operating under a corporation (company) or partnership entity, they are specifically excluded from being classified as an employee of your business.

How Premiums Work

Once you have identified who you are required to cover, the next step is understanding what type of cover must be provided. Employees may be suited to ‘Household workers’ or ‘Volunteer’ insurance but most employees will require ‘Accident insurance’.

An ‘Accident insurance’ policy will cover you if one of your employees experiences a work-related injury or illness and needs to claim workers’ compensation. The policy includes cover for both no-fault statutory claims and damages (at-fault) claims. The cost of Workcover regardless of the policy is broken into a premium and excess element like most insurance.

The premium for a standard accident insurance policy cost will depend on several things:

- the amount your business pays in wages.

- your claims experience (the cost of any injury claims against your business)

- your industry.

Premiums are usually paid ’provisionally’, which means you’ll pay a premium amount at the start of the financial year which may be adjusted at the end of the year if needed. The provisional premium amount is calculated using an estimate that the business provides WorkCover, forecasting their employees’ expected wages/salaries. Then at the end of the financial year the business will report actual wages/salaries and the premium will be adjusted according to the variation from the estimate. This process is often referred to as an ‘annual wage declaration’.

Additionally, the business will be required to pay an excess if an employee has taken time off from work due to an injury, AND the employee’s claim is accepted resulting in them receiving weekly compensation.

All this information is important for businesses to understand and implement to ensure they are meeting their legal obligations as an employer. A simple roadmap for implementation has been set out for guidance below.

- From 1 July – declare your wages, this will include.

- Estimated wages for the coming financial year

- Actual wages for the last financial year

- 31 August – wage declarations due

- 16 September – if you pay in full by this date and your wages were declared on time, you’ll receive a discount on your premium.

- 30 September – your full premium payment is due by this date if you don’t have a payment plan.

In June, WorkCover Qld will email you an Interim Certificate of Insurance, that will cover you from 1 July until 30 September. This is to give you clear coverage during the policy renewal season.

Once you have paid your premium for the new financial year or committed to a payment plan, you will receive your Certificate of Currency, which will cover you for the full financial year (from 1 July until 30 June).

Comments are closed.